Shakespeare Blog: View from the Lake

Medicare Planning During Open Enrollment

Written By: Brian Ellenbecker, CFP®, EA, CPWA®, CIMA®, CLTC®

For people enrolled in Medicare or for those soon to be eligible, there is no shortage of planning-related questions that typically come up.

Two often overlooked planning issues are whether you should make any changes to your coverage during open enrollment, and will you be subject to higher Medicare premiums due to having income over a certain threshold. Let’s explore each of these questions individually and use a decision tree to help you determine what path to take.

Changing Your Plan During Open Enrollment

Medicare open enrollment starts on October 15 and runs through December 7. Any changes made during this window take effect on January 1, 2024. If you’re currently enrolled in Medicare, you may be able to make certain changes to your coverage during this window. But how do you know if you should make changes? What things should you consider? Let’s take a look at the flowchart below to help guide you:

If you’re currently enrolled in a Medicare Advantage or Part D plan, your insurer will send you a “Plan Annual Notice of Change” letter (ANOC) in September. The ANOC typically comes with your plan’s Evidence of Coverage, which describes in detail the plan’s costs and benefits for the upcoming year. The ANOC describes any changes in coverage, cost, network of providers, drug formulary, etc. that will take effect in January. It’s important to review this notice to see if your plan will continue to meet your health care needs during the next year.

Down the left-hand side of the flowchart, determine if any of those changes occurred to your current plan. If so, you may need to make a change. The flowchart will walk you through the different options available to you if one of the key components of your plan has changed and when you are allowed to make those changes.

If you do want to explore plans to see if a better fit is available, we recommend working with an insurance agent who is an expert in Medicare. While tools like the flowchart can get you started, decisions like this typically require a high degree of expertise and familiarity with the plans available to you. If you would like a referral to an agent, please contact your Shakespeare Advisor. They can answer many of your questions and also refer you to an agent that can help you find a new plan.

Income Related Monthly Adjustment Amount (IRMAA) Planning

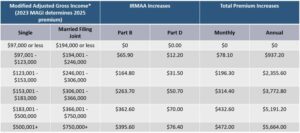

Premiums for Part B and Part D plans are means tested, meaning once your income reaches a certain level, you will pay more in premiums. Income thresholds and per-person premium amounts for the 2023 plan year are shown on the table below:

Tax Planning with IRMAA

CMS estimates that about 7% of Medicare beneficiaries pay IRMAA. There is some planning that can be done to potentially reduce or avoid the impact of IRMAA.

The flowchart below can help you determine whether or not you will be subject to IRMAA and whether or not you might be able to appeal that decision.

The income used to determine your Medicare premiums is based on the income from your tax return from two years ago. 2023 premiums were based on 2021 income. 2023 income will be used to determine 2025 premiums. Because of that, Medicare income planning may need to start as early as age 63, assuming you plan to enroll in Medicare at 65. When you’re 65, your age 63 income will determine your first year of Medicare premiums.

Your income is reassessed every year. If your income fluctuates enough to move between different brackets, your premium will also adjust. The good news is that if you have a temporary spike in income that only lasts one year. For example, you will only pay higher Medicare premiums once, assuming your income drops back down to its prior level.

If you experience a “life changing event” that results in a decrease in your income, you may be able to appeal the IRMAA assessment. A list of lifechanging events can be found on page 2 of Form SSA-44, which is the form used to file an income appeal with Medicare based on one of these events:

Work Reduction and Work Stoppage are two that many people often overlook. If you retire, or at least work less than you did previously as you transition to Medicare, you do not have to include the employment income you previously earned when calculating your Medicare premium, assuming you don’t plan to resume working. By not needing to count prior employment income, many people who were high income earners while they were working will see their current income drop to a level low enough to avoid paying IRMAA once they retire.

Your Shakespeare financial advisor or your tax advisor can help you with the tax planning required to manage IRMAA and minimize the impact it will have on your situation. Reach out with any questions as we are here to help provide you peace of mind.